If the United States’ economy were an athlete, right now it would be peak LeBron James. If it were a pop star, it would be peak Taylor Swift. Four years ago, the pandemic temporarily brought much of the world economy to a halt. Since then, America’s economic performance has left other countries in the dust and even broken some of its own records. The growth rate is high, the unemployment rate is at historic lows, household wealth is surging, and wages are rising faster than costs, especially for the working class. There are many ways to define a good economy. America is in tremendous shape according to just about any of them…

The American public doesn’t feel that way—a dynamic that many people, including me, have recently tried to explain. But if, instead of asking how people feel about the economy, we ask how it’s objectively performing, we get a very different answer.

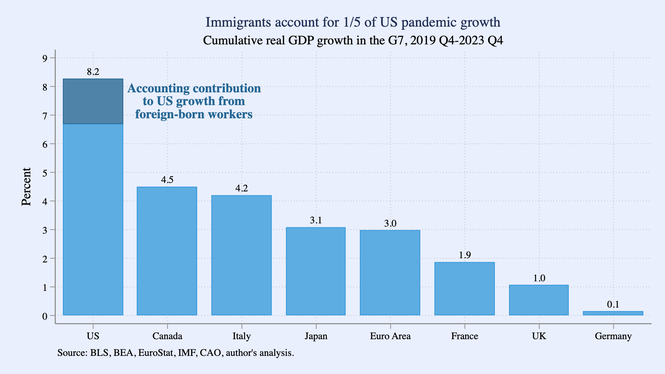

Let’s start with economists’ favorite metric: growth. When an economy is growing, more money is being spent. More stuff is being produced, more services are being performed, more businesses are being started, more workers are being hired—and, because of this abundance, living standards are probablyrising. (On the flip side, during a recession—literally, when the economy shrinks—life gets materially worse.) Right now America’s economic-growth rate is the envy of the world. From the end of 2019 to the end of 2023, U.S. GDP grew by 8.2 percent—nearly twice as fast as Canada’s, three times as fast as the European Union’s, and more than eight times as fast as the United Kingdom’s.

“It’s hard to think of a time when the U.S. economy has diverged so fundamentally from its peers,” Mark Zandi, the chief economist at Moody’s Analytics, told me. Over the past year, some of the world’s biggest economies, including those of Japan and Germany, have fallen into recession, complete with mass layoffs and angry street protests. In the U.S., however, the post-pandemic recession never arrived. The economy just keeps growing.

Source: Briefing Book

Still, growth is a crude measure that says very little about people’s day-to-day lives. Perhaps the right question to ask is: Are most Americans better off financially than they were before the pandemic? …

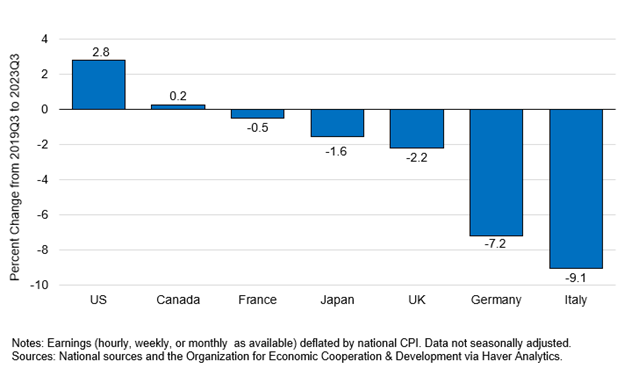

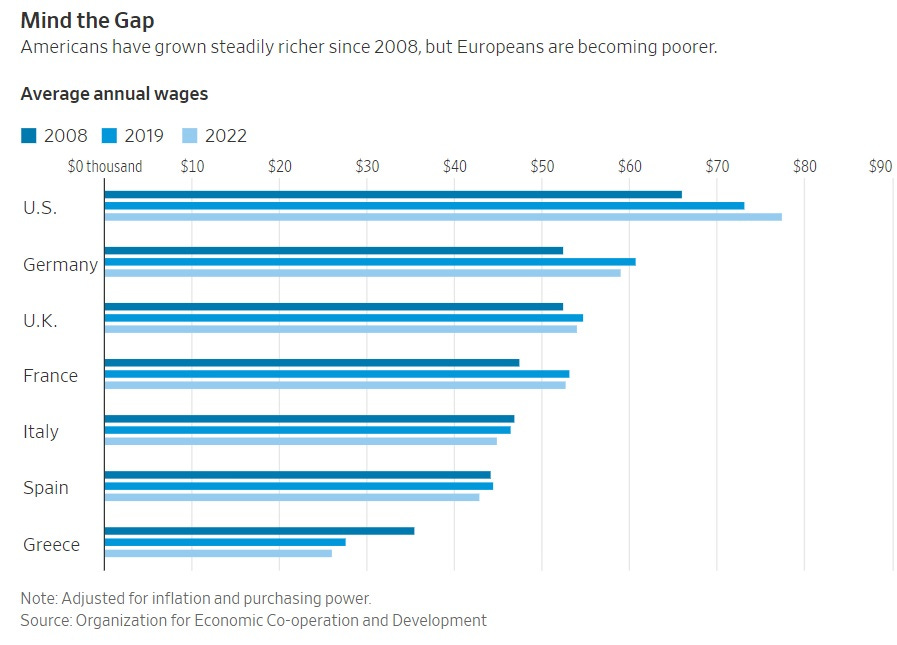

Other nations probably wish they had the luxury of debating such technicalities. From the beginning of the pandemic through the fall of 2023, the last period for which we have good comparative data, real wages in both Europe and Japan fell. In Germany, workers lost 7 percent of their purchasing power; in Italy, 9 percent. By these metrics, the only workers in the entire developed world who are meaningfully better off than they were four years ago are American ones.

Source: US Department of the Treasury

Averages can conceal a lot, of course. The rise in inflation-adjusted wages, which economists call “real wages,” might not be such good news if it were flowing mostly to the already-wealthy, as it did during the recovery from the Great Recession. In fact, from 1964 through 2018, real wages for most workers hardly budged; almost all gains went to the richest Americans. In the early days of the pandemic, when millions of low-income workers found themselves suddenly out of a job, it would have been reasonable to expect the same trend to play itself out…

Instead, the opposite happened. A recent analysis from the Economic Policy Institute found that from the end of 2019 to the end of 2023, the lowest-paid decile of workers saw their wages rise four times faster than middle-class workers and more than 10 times faster than the richest decile.

So, what’s the problem with perceptions?

Indeed, the out-of-control cost of housing is perhaps the biggest black mark on an otherwise excellent economy. This problem started decades ago—since the 1980s, the median U.S. home price has increased by more than 400 percent, twice as fast as incomes—and got even worse during the pandemic, as the rise of remote work prompted millions of people to seek more space. Those rising prices have collided with higher interest rates to produce the most punishing housing market in at least a generation. Would-be homeowners can’t afford to buy, and many existing homeowners feel stuck in place.

Ezra Klein and Annie Lowrey had a great discussion about this on his podcast this week.

Annie Lowrey

Both you and I became reporters during the George W. Bush administration. And I was doing a lot of intense beat reporting during the Obama administration. And throughout this entire period, and this is what people are experiencing in the economy, the economy is defined by low growth, low interest rates, low inflation, high inequality. And the primary problem that policymakers are trying and failing to solve has to do with consumer demand, with demand in the economy. The issue is that people aren’t making enough money to buy things.

This entire time, this cost of living crisis is also brewing. And you can even date it somewhat earlier, but I think probably, the aughts are a good place to start it, where the cost of — I identify four things, but there are probably five. These are costs that are big and are sticky, and that you are not transacting frequently. And the four things are health care, child care, higher ed, so higher ed debt, and then housing. And the cost of all four of those things becomes really, really brutal, not just for low income Americans, but middle income, and in some cases, even upper-middle income Americans.

And it really changes our relationship to the economy. And it sneaks up on us again because we’re in this circumstance in which the primary issue is wages and low demand.

And Karma’s article had this, but it’s a really important point just how great we are doing compared to other countries. Noah Smith:

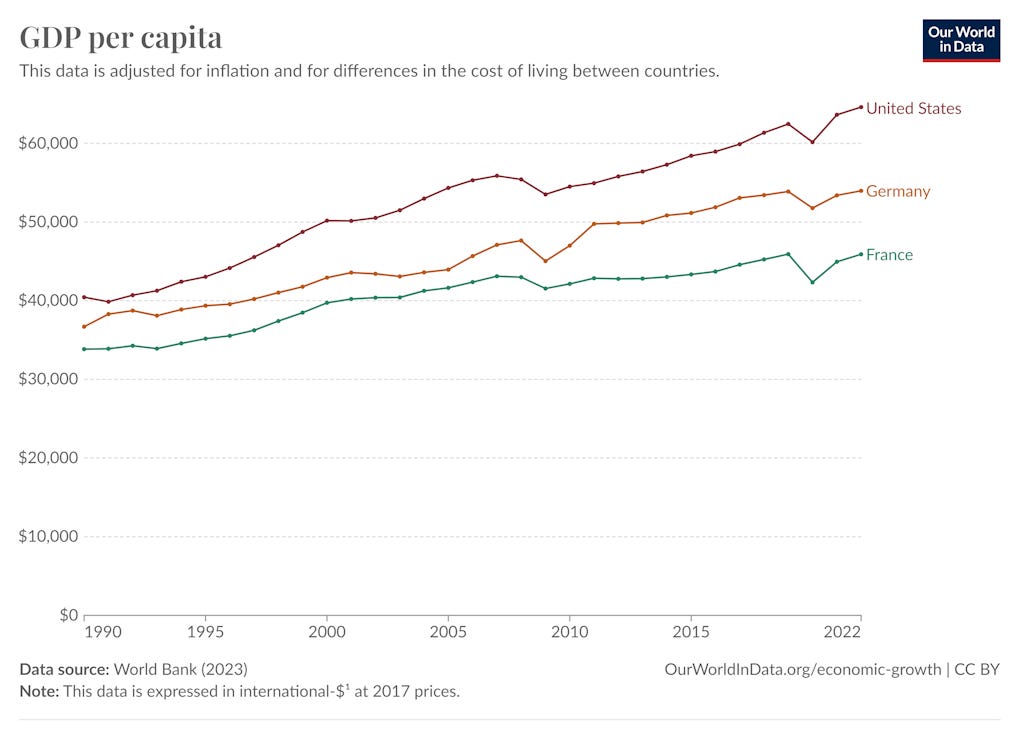

Although East Europe has seen robust catch-up growth, living standards in the core European economies of France and Germany have been lagging behind the U.S.:

In 1990, France’s per capita GDP was 83% of the U.S. Now it’s down to 71%. And the divergence has only accelerated since the pandemic, with the U.S.’ recovery outpacing Europe’s by leaps and bounds:

And, lastly, Kevin Drum with a great point on the inflation that surely has been a major factor in Biden’s unpopularity:

Europe measures inflation using something called HICP—the Harmonized Index of Consumer Prices. This is measured a bit differently than CPI in the United States, but luckily the BLS calculates an unofficial HICP index for the US every month. This allows an apples-to-apples comparison of inflation in the US and Europe. Here it is:

It should surprise no one that inflation is pretty closely matched. In particular, our recent inflationary surge happened almost identically in Europe with a lag of a few months. This is why you shouldn’t pay much attention to anyone who suggests there was some kind of unique American action that caused inflation. It was a worldwide phenomenon and that points in pretty much one direction: COVID.

It wasn’t Joe Biden’s stimulus. It wasn’t greedy American companies. And it wasn’t anything special about our response to COVID. It was supply constrictions caused by the pandemic combined with government actions to keep incomes stable. Reduced supply + stable demand = inflation. Simple.

In a rational world, sure we would be working on policies for housing problems, etc., but with this economy, Biden should be cruising to a re-election. As has been well-documented, we don’t live in a remotely rational world.

It should surprise no one that inflation is pretty closely matched. In particular, our recent inflationary surge happened almost identically in Europe with a lag of a few months. This is why you shouldn’t pay much attention to anyone who suggests there was some kind of unique American action that caused inflation. It was a worldwide phenomenon and that points in pretty much one direction: COVID.

Recent Comments